Every retail and e-commerce company runs on software it rarely talks about in public. The brand, the storefront and the marketing get the attention, but the real operating system is the stack of tools and vendors sitting behind the scenes: the commerce platform, the payment processor, the warehouse management system, the data layer and the dozens of point solutions that connect them. In 2026 that stack is no longer a back-office concern. It is the difference between a company that ships on time and one that bleeds margin on every order.

This guide walks through the tools and vendors that matter for a retail or e-commerce company in 2026, what each layer actually does, where teams overspend, and how to build a stack that scales without locking you into a single supplier. It is written for operators who have to make these calls, not for procurement theater.

In short

- The stack has consolidated, not simplified. Fewer vendors now own more of the workflow, so each contract carries more switching risk.

- Commerce platform, payments and data are the load-bearing layer. Get these three right and the rest of the stack becomes replaceable.

- AI moved into the core in 2026. Merchandising, support and forecasting tools now ship machine learning as a default feature rather than a paid add-on.

- Total cost of ownership beats sticker price. Integration time, payment fees and staffing usually dwarf the license cost you negotiate.

- Avoid single-vendor lock-in. The companies that survive supplier price hikes keep their data portable and their integrations standards-based.

Why company tooling matters more in 2026

For most of the last decade, retail technology budgets grew on autopilot. Margins were healthy enough that a redundant subscription or a clunky integration was an annoyance rather than a threat. That cushion is gone. Grocery and general merchandise margins have compressed, consumer spending has cooled in several US categories, and the cost of capital makes every recurring contract a line item that finance now reads closely.

The result is a sharper question in every boardroom: which tools actually move revenue or protect margin, and which are just habit. A company that answers that question well can redirect spend toward the systems that compound, such as data infrastructure and conversion tooling, and away from the ones that simply keep the lights on. A company that answers it badly carries dead weight into a tighter market.

There is a second reason 2026 is different. The tooling landscape has consolidated. Payment networks, commerce platforms and logistics providers have been buying each other for two years, which means the vendor you sign today may be owned by a competitor of your other vendors tomorrow. That changes how you negotiate and how much portability you should demand up front. To see how that news flow shapes operating decisions, our pillar guide on how retail news shapes the global e-commerce industry maps the signals that should feed your vendor strategy.

What changed between 2024 and 2026

Three shifts define the current moment. First, AI features that were premium add-ons in 2024 are now bundled into core platforms, which resets what you should pay for them. Second, real-time data has become table stakes, so batch-only tools look dated. Third, payment economics have moved to the center of vendor selection because processing fees are one of the few large costs a growing company can still negotiate.

Key terms and definitions

Before comparing vendors, it helps to agree on language. The same word means different things to a platform sales rep and to your engineering lead, and that gap is where bad contracts get signed.

A commerce platform is the system that renders your storefront, manages the catalog and processes the cart. A payment processor moves money from the shopper to your bank and handles fraud, settlement and refunds. A headless setup separates the storefront a customer sees from the commerce engine behind it, so you can change one without rebuilding the other.

An order management system, often shortened to OMS, is the brain that decides which warehouse or store fulfills each order. A warehouse management system, or WMS, runs the physical operation inside that building. Retail media is the advertising business a retailer builds on its own site and shopper data, and it has become a meaningful profit line for larger companies.

Finally, total cost of ownership, or TCO, is the full cost of running a tool over its life: license, integration, training, support and the staff time to operate it. Sticker price is usually the smallest part. Understanding how a company is structured to make these calls is its own subject, which our breakdown of the org chart of a typical large retail company covers in detail.

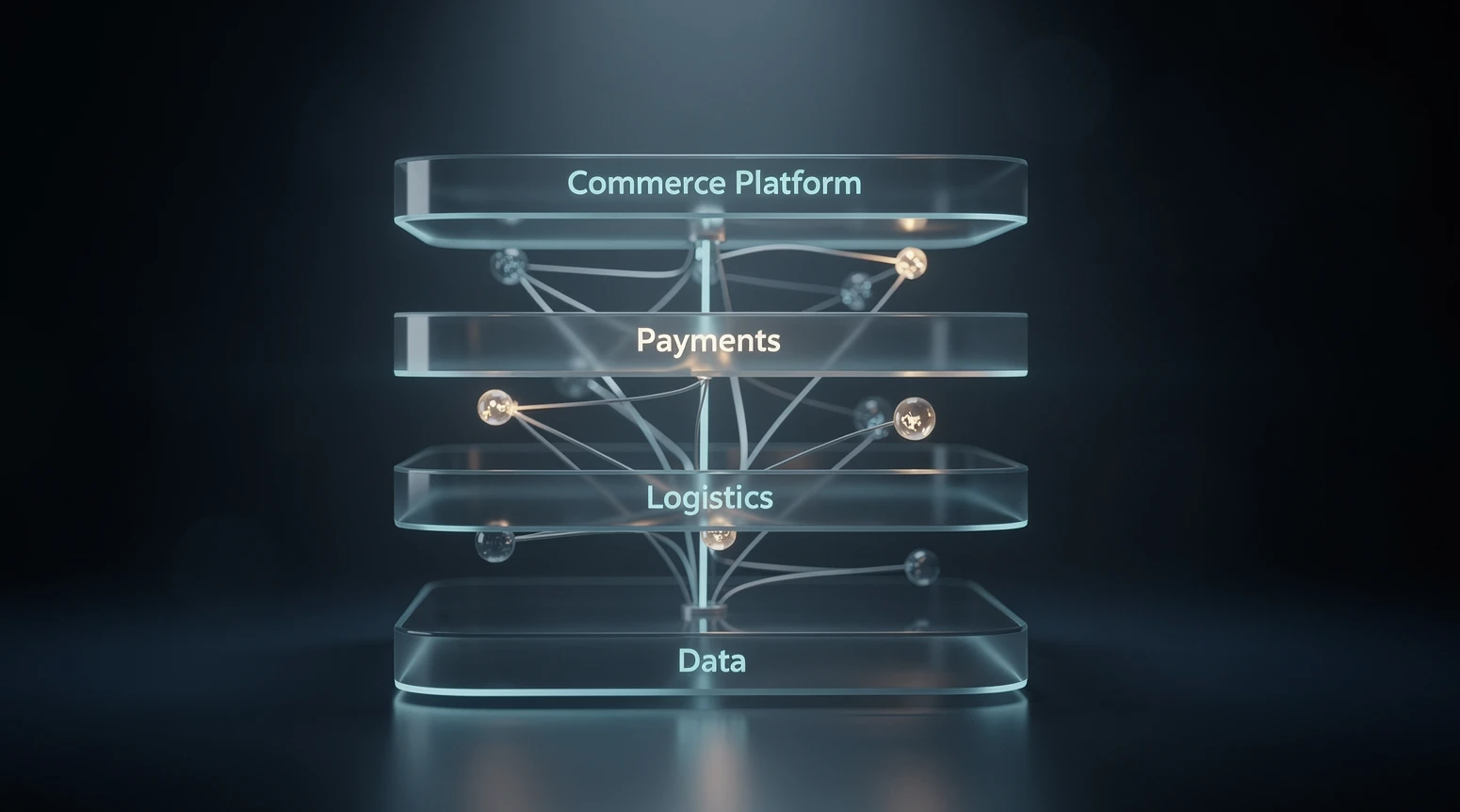

How the modern retail tool stack works in practice

A useful way to picture the stack is as four layers stacked on top of each other, each depending on the one below. The bottom layer is data and identity: who your customers are, what they bought and what your inventory looks like in real time. Nothing above it works well if this layer is wrong.

The second layer is the transaction engine: the commerce platform and the payment processor that turn a browsing session into money in the bank. The third layer is fulfillment: the OMS and WMS that get the product from a shelf to a doorstep. The top layer is growth: marketing, retail media, analytics and the customer support tools that bring shoppers back.

The mistake most teams make is buying the top layer first because it is the most visible, then bolting it onto a weak foundation. A best-in-class advertising tool cannot fix bad inventory data. The companies that scale cleanly invest in the bottom two layers early, then add growth tools once the foundation can support them.

Why integration is the real cost

Any individual tool can look affordable on its pricing page. The cost shows up when you connect it to the rest of the stack. A payment processor that does not talk to your OMS creates manual reconciliation work. A loyalty tool that cannot read your real-time inventory promises rewards on products you cannot ship.

This is why standards matter. Vendors that expose clean APIs and support common data formats cost less to live with, even when their license is pricier. Vendors that trap your data in a proprietary format charge you twice: once for the subscription and again when you try to leave. Budget for integration as a first-class line item, not an afterthought.

The core stack: platforms, payments and data

The table below maps the load-bearing layer of a 2026 retail stack. These are the three categories where a wrong choice is expensive to reverse, so they deserve the most scrutiny during selection.

| Layer | What it does | What to optimize for | Typical risk if you get it wrong |

|---|---|---|---|

| Commerce platform | Storefront, catalog, cart and checkout | Flexibility, API quality, total cost at scale | Re-platforming projects that run over a year and stall growth |

| Payment processing | Authorization, settlement, fraud, refunds | Effective fee rate, approval rates, global coverage | Margin leakage of 1 to 3 percent of revenue on fees alone |

| Data and identity | Customer profiles, inventory, order history | Real-time accuracy, portability, privacy compliance | Every downstream tool inherits bad data and bad decisions |

| Order management | Routing orders to the right location | Inventory visibility, rules engine, store fulfillment | Oversells, split shipments and rising delivery cost |

Note how payment processing sits in this group. For a company doing meaningful volume, a half-point improvement in effective fee rate can fund an entire other tool. That is why payment economics now drive vendor talks rather than sitting at the end of them. The recent wave of payment deals, such as Deluxe buying Celero Commerce, shows how quickly this layer is reshaping itself around merchant volume.

Build, buy or rent

For each layer, the choice is rarely between two named vendors. It is between building the capability in house, buying a packaged product, or renting a service that runs it for you. Building gives control and costs the most in engineering time. Renting is fastest and cheapest to start but hands a margin slice to the provider. Buying sits in between and suits companies large enough to operate the tool but not large enough to build it.

The right answer depends on whether the capability is a differentiator. If your fulfillment speed is how you win, owning more of that stack can pay off. If payments are simply something that has to work, renting from a strong processor is usually the better trade.

Common mistakes and how to avoid them

The failures in this space rhyme. The same handful of errors show up across companies of very different sizes, and most are avoidable with discipline rather than budget.

The first mistake is buying for the demo rather than the daily reality. A polished sales walkthrough hides the friction of day-to-day operation. The fix is to insist on a trial with your real data and your real team, not a sandbox the vendor has tuned to look perfect.

The second mistake is ignoring TCO. Teams negotiate hard on the license, then absorb a far larger cost in integration and staffing without ever measuring it. The fix is to model the full three-year cost before signing, including the people needed to run the tool.

The third mistake is single-vendor lock-in. It is tempting to buy everything from one suite because the integration is easier on day one. The risk arrives later, when that vendor raises prices or is acquired and you have no leverage. The fix is to keep your data portable and avoid proprietary formats wherever a standard exists.

The accumulation trap

A quieter mistake is letting tools pile up. Each new subscription solves a real problem in the moment, but few are ever retired. Over three years a company can end up paying for several tools that do the same job, none of them fully adopted. An annual stack audit that asks which tools are actually used, and by whom, recovers more budget than most teams expect.

This matters most for growing companies, where the urge to add a tool for every new problem is strongest. The same discipline applies to how a company communicates its plans to the market, a dynamic our guide on how retail companies issue guidance and why analysts care explores from the financial side.

Examples from US retail and e-commerce

Abstract advice is easy to nod along to and hard to apply. A few concrete patterns from the US market make the trade-offs real.

Consider a mid-size apparel brand moving from a single warehouse to a multi-node network. The temptation is to buy a powerful enterprise OMS up front. In practice, the brand that scales cleanly usually starts with its platform’s native order routing, proves the operational model, then upgrades to a dedicated OMS only once order volume justifies the integration cost. Buying the heavy tool too early means paying for capacity that sits idle while the team learns.

Consider a grocery chain weighing a retail media build. The data layer it already owns, every basket and loyalty profile, is the asset. The mistake is treating retail media as a marketing project bolted on top. The chains that succeed treat it as a data project first, because the advertising revenue depends entirely on the quality of the shopper data underneath.

A third pattern comes from platform upgrades. When a major commerce platform ships AI merchandising into its core, as seen when Shopify shipped its Summer 2026 editions, the smart move for many companies is to drop a separate paid merchandising tool they were already buying. Bundled features reset what you should pay for standalone point solutions, and teams that audit their stack against platform releases routinely cut spend.

What the winners do differently

Across these examples, the companies that come out ahead share three habits. They invest in the data layer before the growth layer. They review their stack against vendor release notes so they stop paying for features that became free. And they keep at least one realistic exit option for every critical vendor, which keeps pricing honest at renewal.

Tools, partners and vendors worth knowing

Rather than name specific products, which date quickly, it is more useful to map the categories of vendor a 2026 company should have a view on, and what to look for in each. The table below is a checklist for building or auditing a stack.

| Category | Role in the company | Key question when selecting |

|---|---|---|

| Commerce platform | Runs the storefront and checkout | Can we customize without forking the codebase? |

| Payment processor | Moves and protects money | What is the true effective rate at our volume? |

| Logistics and fulfillment | Gets product to the customer | Does it give real-time inventory across all nodes? |

| Retail media and ads | Turns shopper data into ad revenue | Does it respect privacy rules in our markets? |

| Analytics and BI | Tells you what is working | Can non-technical staff actually use it? |

| Customer support | Handles questions and returns | Does AI triage reduce cost without hurting trust? |

| Automation and warehousing | Cuts the cost of moving goods | What is the payback period on the capex? |

Two categories deserve a closer look in 2026. Automation is one. As labor costs rise, more US companies are weighing warehouse robotics, and the surge in spending is real, as our coverage of the US retail automation capex wave documents. The discipline here is to measure payback in months, not to buy automation for its own sake.

The second is the fast-moving world of pop-up and experiential retail tooling, where brands test new markets cheaply before committing to stores. The way D2C brands use pop-ups to test new cities shows how lightweight tooling can de-risk expansion that once required heavy infrastructure.

How to budget for vendors in 2026

A simple budgeting rule keeps the stack honest. Split spend into three buckets: keep-the-lights-on tools that must work, growth tools that should pay for themselves in revenue, and experimental tools on a short leash. Cap the experimental bucket, measure the growth bucket against revenue, and renegotiate the keep-the-lights-on bucket every renewal.

The goal is not to spend less for its own sake. It is to make sure every dollar is buying either reliability or growth, with nothing in between. Companies that run this discipline tend to find ten to twenty percent of stack spend that can be cut or redirected without losing any capability they actually use.

How to choose a vendor without regret

When it comes to a specific decision, a short checklist beats a long evaluation document. Five questions filter out most bad choices before a contract is signed.

- Does it solve a problem we have measured, not one a sales deck invented?

- What is the full three-year cost, including integration and staffing?

- How hard is it to leave, and is our data portable if we do?

- Does it integrate with the two or three systems it must talk to today?

- Who owns the vendor, and could that change against our interests?

If a vendor scores poorly on the last two questions, treat the deal with caution no matter how good the product looks. Switching cost and ownership risk are the factors that turn a good 2026 decision into a painful 2028 one. The consolidation sweeping through retail and payments makes that ownership question more urgent than it was even a year ago.

Where the retail tool stack goes from here

The direction of travel for 2026 and beyond is clear, even if the timing is not. Three forces are pulling the stack in the same direction: deeper AI inside core platforms, tighter integration between payments and commerce, and growing pressure to prove the return on every tool.

AI is the most visible. In 2024 a company might pay a separate vendor for demand forecasting, another for support automation and a third for merchandising. By 2026 those capabilities increasingly ship inside the commerce platform itself. That does not make the standalone tools worthless, but it raises the bar for what they must do to justify a separate line item. The practical effect is that the best forecasting tool now has to beat a free feature, not an empty slot.

Payments and commerce are converging just as fast. Processors are buying commerce capabilities and platforms are building payment products, which blurs a boundary that used to be clean. For a company, that convergence can be convenient or constraining depending on how the contract is written. The same portability discipline that protects you elsewhere matters doubly here, because bundling payments into your platform deepens the lock-in if you ever want to move.

The labor picture is the third force. US warehouse and fulfillment wages have climbed steadily, and federal data from the Bureau of Labor Statistics shows how those costs feed directly into the case for automation tooling. When labor is expensive, a robot with a two-year payback looks very different than it did when wages were flat. That math is why automation has moved from a coastal experiment to a mainstream budgeting question.

Building a stack that survives the next acquisition

Given all of this, the resilient strategy is not to pick the perfect vendor today. It is to build a stack that can absorb change. That means keeping your customer and inventory data in a layer you control, favoring standards over proprietary formats, and treating every critical vendor relationship as one you may have to exit. The companies that do this are not the ones with the flashiest tools; they are the ones that can swap a supplier without rebuilding their business.

None of this happens in a vacuum. Vendor moves, acquisitions and platform releases are news events, and reading them well is how operators stay ahead of their own stack decisions. Our pillar guide on how retail news shapes the global e-commerce industry is the place to track those signals and connect them back to the tooling choices in front of you. The companies that treat news as an input to strategy, rather than background noise, are the ones that buy and cut tools at the right moment.

Frequently asked questions

What tools does a retail company actually need to start in 2026?

At minimum, a commerce platform, a payment processor and a way to track inventory in real time. Everything else, from retail media to advanced analytics, is an addition you layer on once those three work reliably. Starting with the growth tools before the foundation is the most common and most expensive early mistake.

How much should a company spend on its technology stack?

There is no single percentage, because it depends on margin structure and growth stage. A more useful frame is to split spend into reliability, growth and experimental buckets, then make sure every dollar buys either stability or measurable revenue. Companies that audit annually usually find spend they can cut without losing capability.

Is it better to buy one all-in-one suite or several best-in-class tools?

A suite is easier on day one and riskier over time, because it concentrates your switching cost in a single vendor. Best-in-class tools cost more to integrate but keep pricing honest at renewal. The right answer depends on whether a given capability is a differentiator for your business or simply has to work.

Why do payments matter so much in vendor selection now?

Because processing fees are one of the largest costs a growing company can still negotiate, and a small improvement in the effective rate can fund other tools outright. The wave of payment industry consolidation in 2025 and 2026 has also reshaped who owns the rails, which changes leverage at the negotiating table.

How do I avoid getting locked into a single vendor?

Demand data portability in the contract, favor vendors that use common standards over proprietary formats, and keep at least one realistic alternative for every critical system. Lock-in is rarely a problem on day one; it becomes one at renewal, when a vendor knows how hard you are to move.

Should a smaller company build any of its own tools?

Only where the capability is a genuine differentiator. If fulfillment speed is how you win, owning more of that stack can pay off. For commodity functions such as payments, renting from a strong provider almost always beats building, because the engineering time is better spent on what makes you distinct.

How often should we review our technology stack?

At least once a year, and ideally after every major platform release. Vendors regularly bundle features that you may already be paying a separate tool to provide, so an annual audit against release notes routinely recovers budget. The review should ask which tools are actually used and by whom, not just which contracts are due.

What is the biggest tooling risk for retail companies in 2026?

Consolidation. As platforms, payment networks and logistics providers buy each other, the vendor you signed independently may end up owned by a competitor of your other suppliers. That makes ownership and portability the questions that protect you most, even more than price.